Having the right home insurance coverage is key to protecting one of the most significant investments in your lifetime. The average home insurance cost in Ontario varies greatly depending on where you live, the value of your home, your insurance history, and many other factors. Insurance companies calculate your premium based on your actions to maintain your home. However, they can also raise your rates if you don’t. Let’s look at the factors determining your home insurance premiums and how not maintaining your home can affect your premiums, too.

What Is a Home Insurance Premium?

Your home insurance premium is the amount you pay an insurance company to insure your home. Your home insurance premium is generally calculated for one year and can be paid monthly, at determined periods, or in a one-time payment.

How Are Home Insurance Premiums Calculated?

Home insurance premiums are calculated based on several factors, each of which rates your risk of having an insured loss. Some of the factors that determine a home insurance premium include:

- Location of your home

- Your home’s Replacement Cost Value

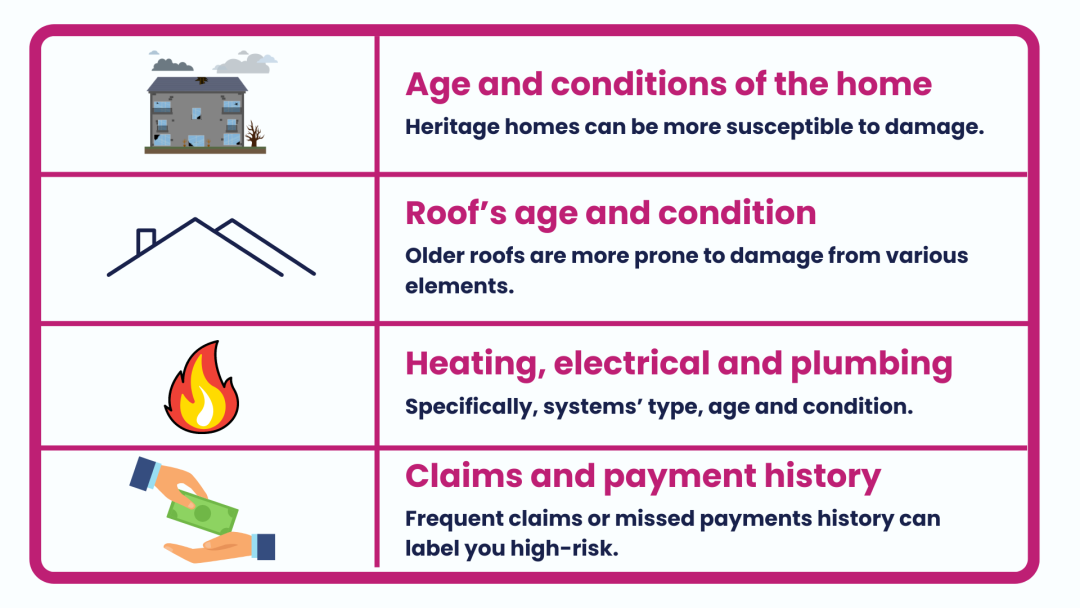

- The age of plumbing

- Electrical services in the house

- The condition of the roof

- Distance from a fire hall or fire hydrant

- Your claims history

- Your insurance history

Ontario homes differ in many ways, such as their age, condition, and size. Many homeowners don’t realize how these differences affect their home insurance premiums. If your home is deemed high-risk, you may not be able to get standard home insurance and will have to look to specialized high-risk insurers to get coverage.

Several factors can make Ontario home insurers deem your home a high-risk property. Understanding these factors is critical for Ontario homeowners. They significantly affect your coverage options and home insurance costs. Here are some key elements that insurers look at to determine if a home is high-risk:

- Age and condition of the home: Older or poorly maintained homes are more susceptible to damage and may be considered high-risk by home insurers. Condition-related issues, such as deteriorating roofing and outdated plumbing, can lead to higher premiums or denial of coverage under a standard policy.

- Location and environmental factors: Homes in areas prone to natural disasters or regions experiencing extreme weather events due to climate change may be considered high-risk.

- History of missed payments and/or multiple claims: If you lapse in coverage, miss multiple premium payments, or file many claims quickly, this increases a home insurer’s perceived risk of insuring your property.

- Home usage: Homes that aren’t regularly occupied by their owners can be considered high-risk, such as vacation homes. Vacant homes are also considered high-risk because no one regularly monitors the property, making it susceptible to theft, vandalism, and damage from a lack of home maintenance.

- Crime rate: Homes in neighbourhoods with high crime rates may be deemed high-risk because of the increased likelihood of crimes resulting in damage to or loss of the home and the homeowner’s belongings.

Climate change has significantly affected the home insurance market through the increased frequency and severity of natural disasters, like storms and floods. The Insurance Bureau of Canada reported $3.1 billion in insured damages from natural catastrophes in 2023, making it the fourth-worst year for insured losses in Canada.

Maintaining Your Home Can Affect Your Premiums

There are numerous steps you can take to reduce your risk of exposure to losses and damages. These measures can also help to reduce your home insurance premium. Some damage prevention steps and mitigation devices include:

- Keeping your home well maintained. Fix a leaky roof or pipe, maintain a fence around your pool, prevent damage by rodents and other vermin, and keep up with other home maintenance. You reduce the risk of a loss with well-maintained premises.

- Reinforce your roof. Replace old shingles with more impact-resistant materials to reduce the risk of leaks and prevent storm damage.

- Conduct regular home maintenance. Regularly checking for issues and repairing them ASAP can prevent minor issues from causing significant damage that may lead to insurance claims.

Owners of brick homes, newly-built homes, or homes of fire-resistant materials generally pay lower home insurance premiums. The home insurance premium will likely increase as a home ages.

- Enhance your home security. Many home insurers offer discounts if you implement home security measures to deter theft and vandalism, such as deadbolt locks, security cameras, and burglar alarm systems.

- Taking steps to reduce the risk of water damage. Water damage is a leading cause of home insurance claims. Reducing the risk of water damage keeps your home safer and lowers your home insurance costs. Installing water sensors, alarm systems, backwater valves, and alarmed sump pumps are all great damage prevention and mitigation devices.

- Maintain proper yard upkeep. Maintain landscaping, improve drainage, and keep walkways neat. Regularly trim your trees to prevent the risk of branches falling during a storm and damaging your home. These measures will reduce the risk of damage related to risks like flooding and storms.

- Add fire safety improvements. Installing fire safety features such as smoke detectors and sprinkler systems reduces the risk of fire-related claims and may persuade your insurer to discount your premiums.

- Upgrade your electrical and heating systems. Old systems can increase the risk of incidents like fires caused by electrical damage. Aluminum or knob-and-tube wiring increases the risk of fire. Upgrading to newer, more efficient systems not only makes your home safer it also leads to lower home insurance premiums.

- Update your plumbing: Homes with copper or plastic piping get better insurance rates because galvanized or lead piping means old plumbing with a higher risk of cracks and leaks. Updating your plumbing can reduce your risk related to water damage.

Year-Round Maintenance

As a homeowner, maintaining your property is your responsibility. So, if you neglect your property, allowing it to fall into a state of disrepair, and a loss or damage occurs, your home insurance company can cancel your policy. Or, at the very least, deny your claim. Not maintaining your home can affect your premiums, therefore year-round property maintenance is important if you want to avoid a canceled home insurance policy. Home maintenance can be done independently, or you can hire someone to do it for you. Examples of essential home maintenance include:

- Cleaning the gutters

- Emptying your dryer vent

- Have your chimney and HVAC units inspected annually

- Adopting basic fire safety practices, such as regularly testing your smoke detectors and replacing the batteries as needed.

Remember, it is always a good idea to perform home maintenance checks at least four times a year – with the changing seasons. Though many of us don’t want to think about it, fall is right around the corner. Getting a head start on your fall home maintenance while the weather is warm and dry may be a new habit worth considering. Taking care of your most valuable possessions is essential. Not only to keep you and your loved ones safe but also to help keep your home insurance premiums down. Not maintaining your home can affect your premiums, so it is best to show your home some love.

To ensure you pay the lowest premium possible, speak to one of our isure representatives today about your policy. We are happy to advise you regarding further discounts you may be entitled to.

Renovations are exciting! There are so many things to think Read more

With increases in extreme weather across the country, some Canadians Read more

Currently, more than 1.5 million households across the country remain Read more